You might’ve seen it called “cash stuffing” on social media. But this low-tech budgeting strategy, also known as the envelope budget system, has been around longer than the internet itself.

A good budgeting system can help you spend more on the things that align with your values and less on the things that don’t, which can help you find more joy and satisfaction in life. So let’s break down how cash stuffing works and explore whether budgeting with envelopes can really help you take more control of your spending.

The highlights:

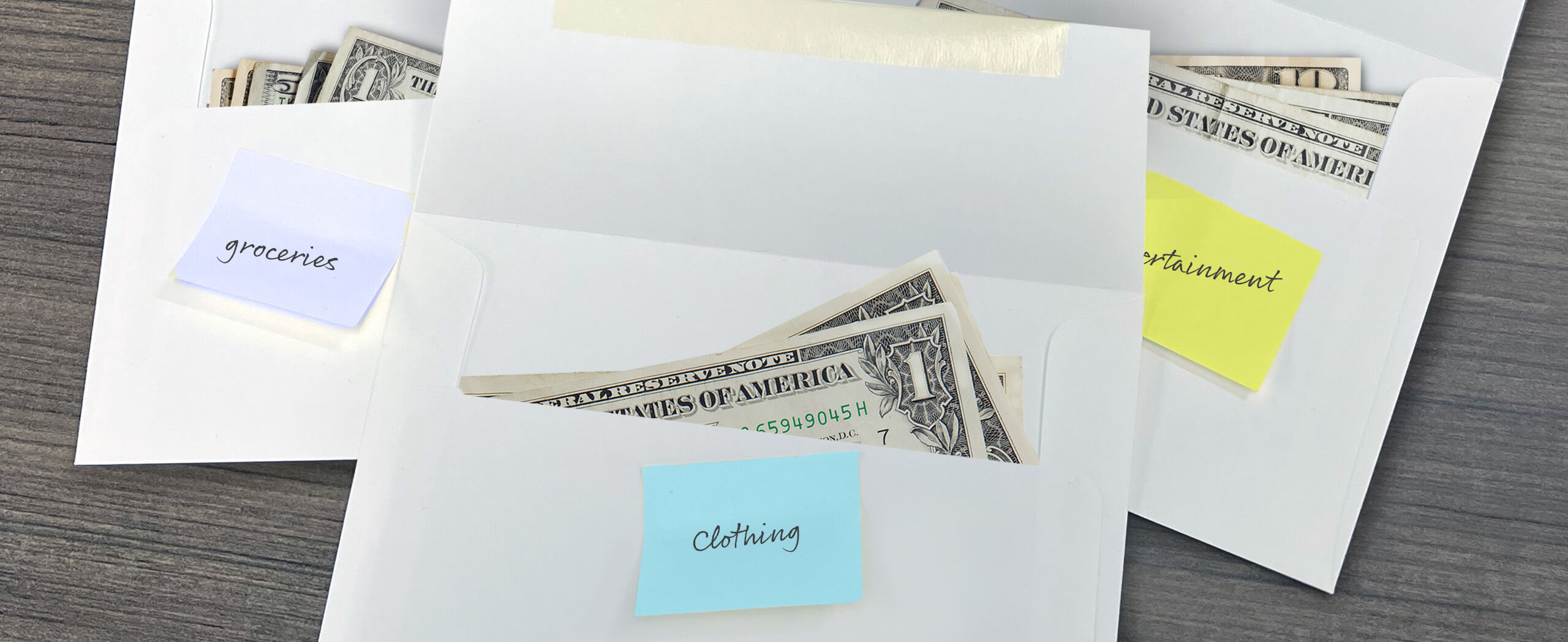

- Cash stuffing describes a budgeting technique that involves keeping your paper money in envelopes labeled with specific spending categories.

- Budgeting with this cash envelope method may help you limit overspending—but keeping too much of your money in cash can keep you away from the benefits of bank accounts, credit cards, and digital finance tools.

- There are also digital envelope systems that adapt cash stuffing principles to fit more naturally with today’s more “cashless” world.

- Whatever budgeting strategy you use, building a spending plan that works for you means figuring out where your money’s going—and deciding where you want it to go.

What is cash stuffing?

The idea behind the cash stuffing envelope system is that physically dividing up your money can help you track your expenses and stay on budget. We’ll get into some digital variations on this old-school technique later, but today’s most popular version of physical envelope budgeting requires two tangible things: cash and envelopes.

In its simplest form, cash stuffing means that after paying your fixed bills (like your rent and phone plan) and setting aside money for savings each month, you divide the rest of your income up as cash. Then you “stuff” the cash into envelopes labeled with various spending categories. If you want to spend $200 a month on groceries, you’ll put $200 cash into the envelope marked “groceries” and pull out some cash whenever you go grocery shopping.

Some other common spending categories for your cash stuffing envelopes might include:

- Gas

- Entertainment

- Eating out

- Travel

- Clothing

- Gifts

Not much has changed with this envelope budget system since it was first used generations ago. It has, however, caught on with age groups that typically use more digital tools. According to one study, about 28% of millennials and Gen Zers surveyed (people aged 18 to 41) have used cash stuffing for everyday purchases.Disclosure 1

How does cash stuffing work?

To better understand how you can start cash stuffing, let’s take it step by step:

To better understand how you can start cash stuffing, let’s take it step by step:

- Build your budget. This can take a little time to figure out, but using some of our budgeting tools and worksheets can help you get started. Remember that many of your fixed monthly payments (including internet service and rent) may only be payable by check or card, and that your savings are likely to be better off in an account where they can grow with interest. For these next steps, consider only using what’s left over after you’ve set aside money for those monthly fixed bills plus savings for emergencies and retirement.

- Create your spending categories. Check your monthly bank statements. What do you spend your money on? You can keep your categories general, but getting more specific may help you keep a closer eye on where exactly your variable spending money goes each month. Instead of a broad category like “shopping and entertainment,” think of more specific labels like “movies,” “drinks,” and “household supplies.”

- Set your spending limits. Decide how much you want to spend monthly in each category. Use this opportunity to think about the things you really value. Shape your spending priorities to reflect those values to make sure you’re spending money mindfully.

- Get organized. This part can be fun, too. You can get a little creative with labeling (and even styling) your money envelopes (or file folders or zipper bags) with their respective categories. Put them somewhere clean, safe, accessible, and private. (You don’t want to lose your cash!)

- Start stuffing. Convert enough of your spending money into cash to stuff your envelopes. Don’t spend any more on a category than what’s in each envelope and try to avoid moving cash from one envelope to the other.

- Watch your progress. Think about your spending as you go along. Are there any categories you want to spend less in? Update your budget accordingly. At the end of the month, consider saving any leftover money or putting it toward a long-term financial goal (like paying down debt) before restuffing your envelopes and repeating the process. Don’t forget to spend a little on the things that bring you joy, too—it’s OK to have an envelope (or two) labeled for “fun”!

Read more: 5 tips for joyfully living within your means

What are the potential benefits of cash stuffing?

If you’re trying to stay out of credit card debt and avoid overdrawing your bank account, sticking to cash may help. Other potential pros of cash stuffing can include:

- Limiting overspending. Research shows that people tend to spend less with paper money than when they use a credit card.Disclosure 2 Using cash for at least some of your day-to-day expenses may help you avoid impulse buys and help you stay more disciplined with your money.

- Getting a clearer picture of your money habits. Knowing how you spend your money is the first step toward making adjustments and better aligning your spending with your goals.

- Growing financial confidence. If you’re just starting to take a more active role in managing your money, cash stuffing can be one tangible way to learn more about budgeting.

What are some possible drawbacks to cash stuffing?

Cash stuffing isn’t for everyone. For one thing, it takes time to withdraw cash and stuff envelopes every month. Other cons are:

- Cash is not protected. Having so much paper money around (even if you’re keeping most of it in a safe at home) may leave you more vulnerable to loss or theft.

- It’s a digital world. When you have to go online to pay everything from your monthly bills to your student loans, cash stuffing may seem less effective for managing your budget—even if you only use it for daily or weekly expenses. In fact, about 41% of Americans say they don’t make any purchases using cash in a typical week, which reflects the convenience of using cards or digital payments in day-to-day life.Disclosure 3

- You can’t collect interest on money in envelopes. Still, one survey found that about one in three millennials and Gen Zers who have tried the cash stuffing method found it useful for saving toward a specific financial goal.Disclosure 1 If you feel like cash stuffing can help you save for something long-term, consider writing down the amount you’re saving each month and putting that number on an envelope labeled with your savings goal—while moving the actual money into an interest-bearing savings or money market account.

Read more: 4 effective strategies to resist impulse buying

Are there digital versions of cash stuffing?

There are several budgeting apps that specifically offer digital takes on cash stuffing. But you can also create your own version of a digital envelope system using tools available through many online banking services, digital wallets, or even old-fashioned spreadsheets.

With a spreadsheet, for example, you can label individual columns (your digital “envelopes”) with spending categories and then put your spending limit (your “cash”) in each respective column. When you spend in a particular category, subtract that amount from your spending limit—and don’t spend any more if you hit zero before the month is over.

When you can check all your “envelopes” by opening an app or spreadsheet on your phone, making mindful spending decisions on the fly could start to feel a little easier than keeping up with a bunch of cash-stuffed envelopes at home. Plus, using a card instead of making most of your purchases with cash can help you build your credit score and earn rewards—as long as you’re budgeting with intention and making your payments on time.

Other advantages of going digital with cash stuffing can include:

- Safety—If you’re carrying less cash, you may worry less about the risk of theft or loss.

- Convenience—You can use a card or make digital payments whether you’re shopping online or in-person—and you don’t have to find the right envelope every time you want to make a purchase.

- Access to digital tools and benefits—Online banking tools and budgeting apps can help you automate many aspects of your finances and track your expenses, while keeping your money in a checking or savings account can provide access to additional benefits and protections.

Is cash stuffing right for you?

When it comes to your long-term financial goals, cash-stuffed envelopes simply don’t offer many of the advantages and protections that bank accounts, credit cards, and digital tools can.

But many of the principles behind cash stuffing—like spending less than you make and keeping tabs on your expenses—are key to developing good money habits. The strategy may also help you stick to a disciplined spending plan.

You could also consider a mixed approach. For example, you could keep your “going out” money in cash—but also have a digital envelope system to track your other monthly expenses and use interest-bearing bank accounts to work toward your long-term savings goals.

What’s most important is that you develop a spending plan that works for you and your budget—and helps you put your money toward the things you really care about.

Next step suggestions:

- Whether you want to try cash stuffing, a budgeting app, or a hybrid approach, pick a budgeting method that you think you’ll enjoy and stick with it. Check out our guide to budgeting for more tools that can help you create a spending plan.

- Review your monthly bank statement and identify some expenses that might be quietly draining your wallet. Are there any streaming subscriptions you wouldn’t miss or fees you didn’t know about?

- If you don’t already have one, consider opening a high-yield savings account to set aside money for emergencies and your long-term goals.