Auto Dealers | December 2025

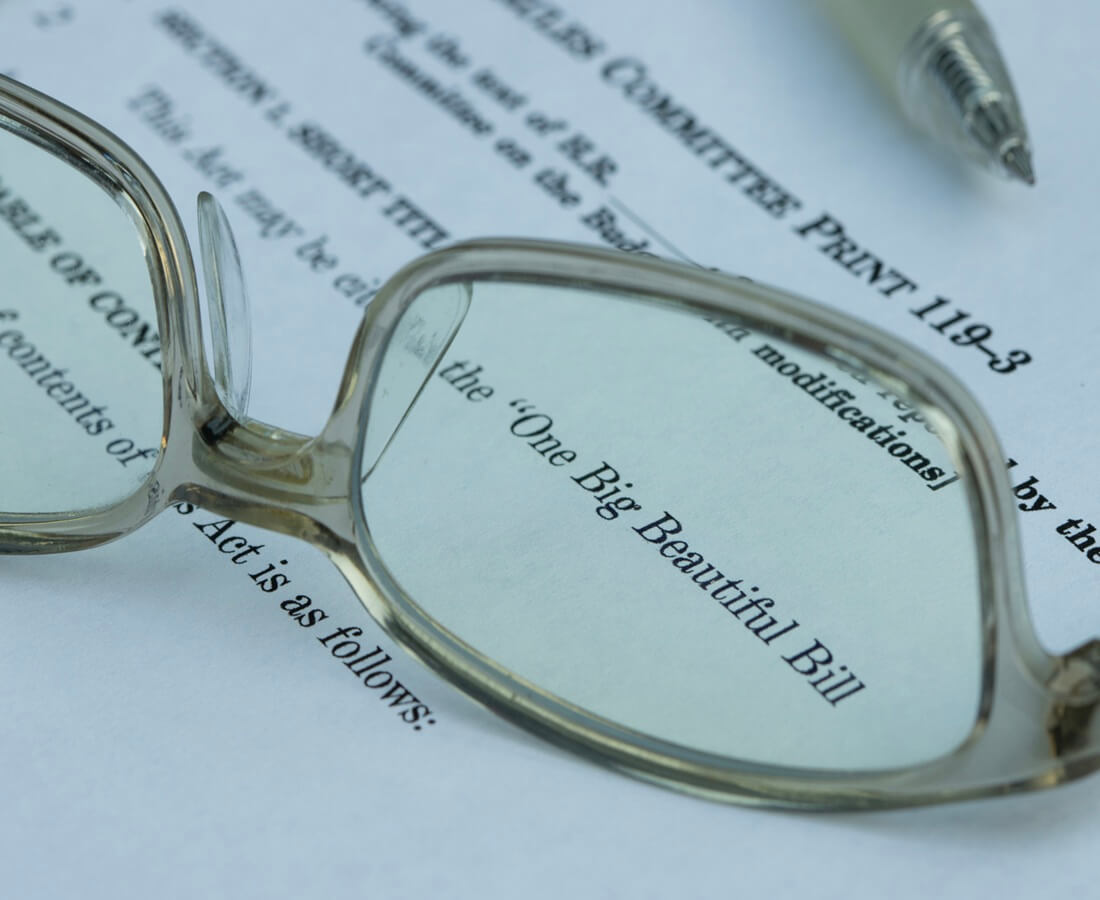

The OBBB and its impact on dealerships

How the OBBB impacts bonus depreciation, floorplan interest deductions, towables, QBI strategies, estate planning, and buy-sell outcomes for auto dealers

Capital Options for Funding Dealership Acquisitions

Auto Dealers Expanded capital options fuel dealership growth

Learn how loan syndications and high-yield debt can provide the capital dealer groups need to fund large-scale growth initiatives.

As the capital needs to support acquisition strategies grow, loan syndications and high-yield debt can provide the flexibility and funding auto retailers need.

Planning for dealership succession

Auto Dealers Planning for dealership succession

Dealership succession planning combines the complexities of maximizing business value with managing family dynamics as owners prepare for a smooth transition that keeps the family and business strong.

Dealership succession planning combines the complexities of maximizing business value with managing family dynamics as owners prepare for a smooth transition that keeps the family and business strong.

Plan now for a smooth business transition later

Auto Dealers Plan now for a smooth business transition later

Learn strategies to avoid 7 common pitfalls when preparing for dealership transition.

Preparing for business transition can help dealerships get ahead of issues when it’s time to exit. Learn strategies to avoid pitfalls when transitioning.