You may be familiar with the idea of a mission statement—a set of guiding principles that can point a business or nonprofit organization toward success. But did you know a family mission statement can do the same thing for you and your heirs?

A family mission statement defines a family’s core values and provides a set of guidelines that can facilitate decision making, enhance communication, and offer accountability for each family member. Sometimes the act of coming together to create one can even spark or renew interest in the family business from members who were disinterested or felt excluded from its operation.

Daisy Medici, managing director of governance and education at the Truist Wealth Center for Family Legacy at GenSpring, recalls a family with four adult children who all participated in the family business. “Two of them eventually left the business because they were unhappy,” she explains. “During the course of our work, we ended up facilitating some amazing family meetings. By engaging the mission statement process and developing several other important guidelines for working together, the family was able to discuss and resolve everyone’s concerns—and those two family members returned to the family business.”

Here, Medici and Carolann Grieve, managing director of family governance at the Truist Wealth Center for Family Legacy, share their insights into what a family mission statement is, how they and their teams work with Truist clients to create them, and how this practice can preserve the wealth and legacy of a successful family business.

How does a family mission statement differ from a business mission statement?

Medici: Most business mission statements are short. Many business leaders believe that if you can’t roll the mission statement off the tip of your tongue, then it’s not effective.

That’s completely different from what we recommend for families. We want family members to identify their purpose as a family and then decide how they can achieve their purpose. We want meat on the bones.

Grieve: I agree. Family mission statements really are much deeper than corporate mission statements. We want family members to base it on the family’s values and purpose—what they want to accomplish with their wealth over time.

How can a family mission statement impact the family business and its legacy?

Medici: There’s an old saying: “Shirtsleeves to shirtsleeves in three generations.” In fact, the odds of sustaining family wealth across multiple generations are as low as 30%.Disclosure 1, Disclosure 2, Disclosure 3 The further a generation gets away from the founding generation, the less connected they are to the story of the founding and the founder’s original values.

One way to defy the odds is to ensure all family members are on the same page when it comes to building, protecting, and transferring wealth to the next generation. That’s where a family mission statement comes in. A family mission statement covers high-level areas that are important to family members—philanthropic interests, family member well-being, education, family cohesiveness, open communication, celebration of individualism, and more.

Grieve: A wealthy family is a business, but we like to call it a family enterprise. A family enterprise encompasses any form of shared assets, whether a family business, a trust with multiple beneficiaries, a vacation home, or a family foundation. Whenever family members need to decide together, it’s important for them to have a family-enterprise perspective. A family mission statement, based on shared values, can help them come to a consensus around their family enterprise.

Who should be part of creating a family mission statement?

Grieve: Best practice is to include everyone who’s an adult—18 or older. Most often, but not always, this includes spouses. Ultimately, the family decides who to include. Everyone who participates takes our proprietary personal values survey, and then our [software] system processes an aggregated list of the family’s shared values. After that, we hold a facilitated meeting to explore those shared values with the family. It’s a great way for everyone to feel included.

Sometimes family members follow other passions and are not involved in the family business. Such choices do not mean they can’t be active in decision-making regarding the greater family enterprise. Being included in family enterprise activities such as the mission statement process lends some transparency into the family business and other shared assets. They start to understand the decisions that are being made—and why they’re being made. This inclusion helps them feel connected.

Medici: Remember, we’re helping families put plans in place to sustain wealth over generations. If all goes well, that wealth is going to get bigger three, four, five generations down the road. With each succession, the family members who are in charge are going to want their next generation of young adult children to be active in the family enterprise. The success in attracting participation could be hindered if someone important to the next generation has been excluded in the past.

Once a family mission statement is created, how do you put it to use?

Medici: In our ongoing work with the family, we keep the mission statement front and center. We use it to develop specific policies that can help them demonstrate the values they’ve identified. For example, if they’ve said they value the connectivity and cohesiveness of the family, how are they going to work together to maintain that?

Grieve: At the Truist Wealth Center for Family Legacy, we have a list of 25 best practices of multi-generational families, and creating a family mission statement is only one of them. Other practices include tactical areas like succession planning, money and relationships, family support network, conflict resolution, and communication. The family mission statement is just one practice that leads to others.

Should the family mission statement come first?

Grieve: We’d like it to. But there are plenty of times when a family will come to us with something they want to address immediately, and we try to customize our approach.

Medici: That said, creating a family mission statement allows them to talk about difficult things that they’ve never been able to talk about as a family. Eventually, they get better at managing those difficult conversations. But not everyone is ready to open the books. If you’re uncomfortable with sharing numbers, what about sharing the flow chart for the estate plan to show the next generation how the money or business ownership will come downstream? Don’t wait too long to talk about that.

How often should it be revisited or revised?

Grieve: There should always be a process for amending the family mission statement. However, we also don’t want to change it willy-nilly because we’re using it as a tool to remind the family of their shared values.

Medici: Some families create an amendment policy that provides guidelines around what it takes to make changes. Family policies aren’t legally binding, but they’re morally binding, and we require that every stakeholder be in the room when these types of decisions are made. If someone can’t attend, we’ll reschedule the meeting.

That sounds like a great way to keep everyone on the same page through generations of decision making.

Medici: It helps keep your family focused on long-term goals, but it also celebrates individualism. Talking about the differences among family members earlier, rather than later, is important.

Grieve: A family mission statement pulls everyone together and helps them understand what their role is within the family business. It creates a space where everyone can work together to create a stronger family enterprise.

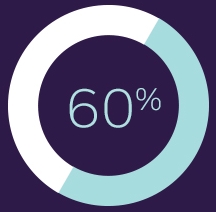

Why can’t families sustain wealth?

of the time it's due to communication and trust issues.

Source: "Shirtsleeves to shirtsleeves: beating the odds of sustaining family wealth," Truist Wealth, accessed July 8, 2022.