A deep bench for your business.

Each client is a big deal. And collaboration around your business matters. So we work as one team at Truist to put industry expertise and the right advisory strategies to bear for you. Plus, with insurance, cash management, and leadership solutions, we simply don’t think you’ll find a better relationship anywhere else.

Staying close to your business is just good business.

Structure and attention matters. We architect a team around your business that knows local and advises with national perspective. And we empower these leaders and teams to provide service that makes sense.

Doing the right thing for the long haul.

We’re about getting to know you and what’s best for your business, not simply focusing on short-term transactions.

Do more—faster. With better technology and proven solutions.

Power and safeguard your company with advanced payments, security tools, cash management options, and consolidated systems.

Commercial banking

Here's what you can expect with Truist. Strategic advice at every stage of your business' lifecycle. Custom financing options to help your business manage cash flow and risk. A partner who sees your vision—and cares to work just as hard to reach it.

Commercial real estate

Capital raising to loan servicing. Private operator to real estate investment trust. Community capital to seniors housing. Whether you need a wide variety of capabilities, efficient decision-making, responsiveness, or specialized expertise, we’ve got you covered.

Corporate and investment banking

Your success is our success—so we’ll do what it takes to get you there. We provide a unique, high-touch advisory approach that stems from a fully integrated corporate and investment banking and sales, trading, and research platform. Our insight and expertise are purposefully designed to align with your strategic objectives, so you can pursue your best future.

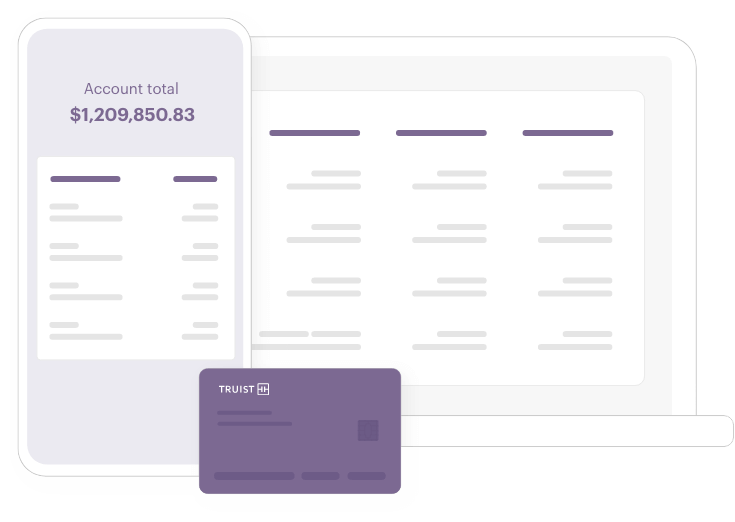

It’s simple. Get a real-time, consolidated view of your accounts and balances—and single sign-on access to multiple banking applications.

We care to keep your accounts safe. Sign in requires a username and password plus a dynamically generated second factor security code.

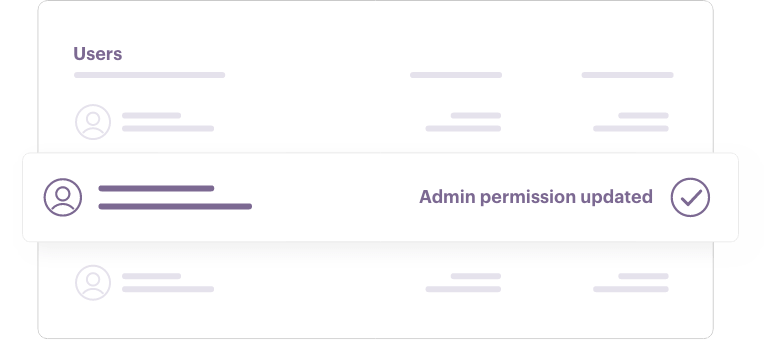

Support your administrators with the features they need to do their jobs—from full system control to permissions set just for them.

Home, office, on the road. Use our mobile app wherever you are to see it all and do it all.