Podcast

Select media

Select category

Podcast: Navigating life’s biggest transitions

Business Owners Episode 44: Navigating life’s biggest transitions

Whether a change helps or hurts, it can be disruptive. Learn how to understand the impact and adapt.

Podcast

07/13/2026

Podcast: Navigating life’s biggest transitions

Hear a clinical psychologist discuss the challenges that even positive life changes can present, and advice for moving forward. | Truist Wealth

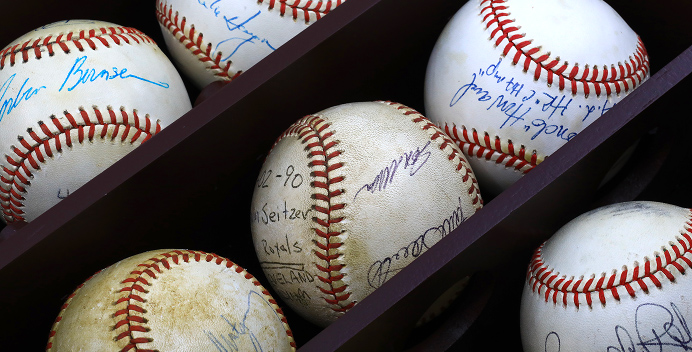

Understanding the Value of Your Sports Memorabilia

Life and Leisure Why collect sports memorabilia: Passion, authentication, value, and possibility

Can rare cards, athlete autographs, and historic gear play a position in your portfolio?

Article

06/12/2026

Article

Explore how sports collectibles fit into a wealth strategy, including risks, returns, authentication, and portfolio diversification considerations.

Podcast: The hidden risk behind business success

Financial Planning Episode 43: The hidden risk behind business success

The unique personal financial risks business owners face—and how planning can help.

Podcast

06/08/2026

Podcast: The hidden risk behind business success

Learn why personal financial planning is challenging for business owners, and explore strategies for addressing business and personal planning together. | Truist Wealth

Episode 42: The trust trap: How scammers target seniors and their wealth

Risk Management Episode 42: How scammers target seniors

Older people can be vulnerable to online scams. Learn how to help recognize and defend against the risks.

Podcast

05/11/2026

Episode 42: The trust trap: How scammers target seniors and their wealth

Learn the ways criminals try to exploit older people online, and how families can better recognize risks and support their loved ones. | Truist Wealth

529 Plan Education Funding: Tax Benefits, Rules, and Planning Strategies

Financial Planning Education funding through a 529 plan

12 questions to ask before opening a 529 account

Article

05/06/2026

Article

Learn how a 529 plan can help fund education with tax advantages, contribution flexibility, beneficiary rules, financial aid considerations, and SECURE Act updates.

Unsecured Lending: A Smart Personal Loan Strategy

Financial Planning 4 reasons to explore unsecured lending

How personal loans can help you increase liquidity without changing your investing plan

Article

04/20/2026

Article

Discover four reasons unsecured personal loans can help you move quickly, access capital, and keep your portfolio intact.

How to Choose the Right Executor for Your Estate

Financial Planning 4 reasons to explore unsecured lending

How personal loans can help you increase liquidity without changing your investing plan

Article

04/20/2026

Article

Learn how to choose an executor for your estate, understand their responsibilities, and decide when to consider professional support.

Mitigating Risks: Why Third-Party Escrow Matters

Attorneys and Law Firms Mitigating risk: Advantages of using independent third-party escrow

Explore the benefits a bank can bring to your next escrow transaction.

Article

04/14/2026

Article

Discover how using independent third-party escrow services can reduce legal risk, prevent fraud, and enhance client confidence.

Podcast: Rethinking Social Security strategy

Investing & Retirement Episode 41: Smart Social Security decisions

Choices that seem small can still impact your future finances. Learn strategies for smart planning.

Podcast

04/10/2026

Podcast: Rethinking Social Security strategy

Understand how Social Security fits into a broader retirement strategy, including tax planning, survivor benefits, and common mistakes to avoid.